Business Policies and Procedures Manual

Cash Handling

(Appendix: Cash Overages and Shortages)

BPPM 30.53

For more information contact:

Controller’s Office

509-335-9651

Contents

1.0 Cash Overages and Shortages

In accordance with state regulations, the University is to ensure that cash overages and shortages are accounted for and posted properly. (SAAM 85.20.10d) Each unit must investigate and correct, if possible, all overages and shortages. Departments are to follow the procedures below to record corrected and uncorrected overages and shortages.

1.1 Departments Not Using University Point-of-Sale System

Department that do not use the University’s point-of-sale system follow the procedures below to document overages and shortages.

1.1.a Overage

If the money (e.g., cash, checks, and credit card receipts) received exceeds the invoice receipts and log sheets, or the ring out on a non-point-of-sale cash register, the department reports the overage amount on a Cash Deposit Report under source-subsource 490-10 using transaction type 01.

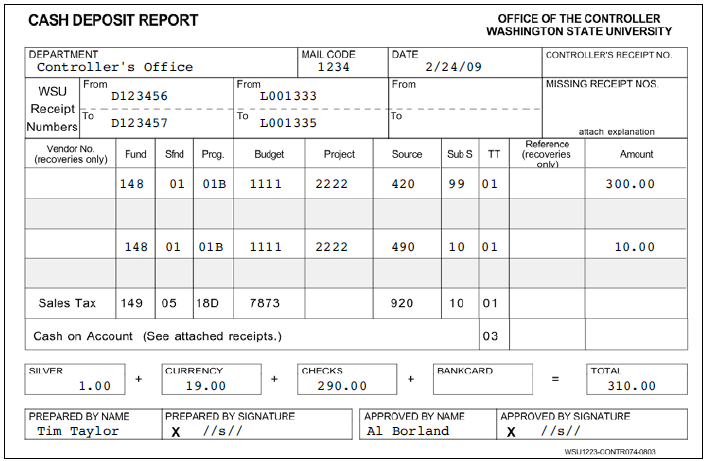

1.1.a.i Example

In Figure 1, the department’s invoice receipts and log sheets total $300.00. The department reports the receipts and logsheets using normal source-subsources, e.g., source-subsource 420-99 (miscellaneous receipts). The till in this example totals $310.00. The department must record the additional $10.00 on the Cash Deposit Report as an overage using source-subsource 490-10.

1.1.b Shortage

If the amount of recorded invoice receipts and log sheets, or the ring out on a non-point of sale cash register exceeds the money received, the department reports the amount short on a Cash Deposit Report under source-subsource 490-11 using transaction type 02. Also, the department must bracket the negative amount to help ensure that the cashier properly records the transaction.

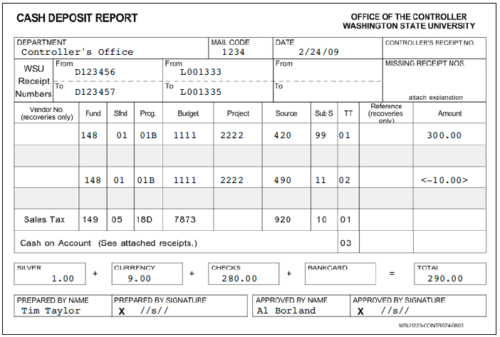

1.1.b.i Example

In Figure 2, the department’s invoice receipts and log sheets total $300.00. The department reports the receipts and logsheets using normal sources-subsources. This example uses source-subsource 420-99, indicating miscellaneous receipts. The till in this example, however, only totals $290.00. The department must record the $10.00 shortage using source-subsource 490-11.

1.2 Departments Using University Point-of-Sale System

The University Point-of-Sale system ceases operations at 4:00 p.m. each day. If departments close early enough, there may be time to correct any discrepancies in order to avoid needing to report overages and shortages. Normally, most point-of-sale locations close at 4:00 p.m., which allows no time to make corrections. University policy requires each department to deposit “intact,” i.e., to prepare the deposit based upon the cash register ring out totals. Therefore, regardless of whether or not an overage or shortage exists, the cash register ring out total is the amount that must be deposited.

1.2.a Till Cash Custodian

The departmental employee who counts the till cash vault, i.e., the till cash custodian, logs and initials any overages and shortages on a vault log sheet.

1.2.b Overage

The department must follow the procedure below to record an overage. If the ring out on the point-of-sale cash register is $1,000.00, but there is $1,010.00 in the till after balancing, the department must deposit $1,000.00 to the bank. The department till cash custodian adds the additional $10.00 to the backroom till cash vault and reports the $10.00 as an overage on a vault log sheet. See Figure 4 for a vault log sheet example. When the department finds and corrects the error on the next day, the department till cash custodian posts the addition of $10.00, which causes a shortage for the second day. If the ring out for the second day is $1,010.00 including the posted $10.00 correction, the till should total $1,000.00 if no other errors occur on day two. The department must deposit $1,010.00 to match the ring out amount. Therefore, the department till cash custodian takes the $10.00 put into the backroom till cash vault on day one and adds it to the day two deposit to cover the shortage. The department till cash custodian reports a $10.00 shortage on the vault log sheet, and the backroom vault is back in balance with the authorized till cash amount (see BPPM 30.51).

1.2.c Shortage

If the ring out on the point-of-sale cash register is $1,010.00, but there is only $1,000.00 in the till after balancing, the department must deposit $1,010.00 to the bank. The department till cash custodian must take the additional $10.00 from the backroom till cash vault and log the $10.00 as a shortage on a vault log sheet. When the department finds and corrects the error on the next day, the addition of a posting of <-$10.00> causes an overage for the second day. If the ring out for the second day is $1,000.00 including the posted negative $10.00 correction, the till should total $1,010.00 if no other errors occur on day two. The department must deposit $1,000.00 to match the ring out amount. Therefore, the department till cash custodian adds $10.00 to the backroom till cash vault to offset the $10.00 taken from the vault on the day before. The till cash custodian reports a $10.00 overage on the vault log sheet, and the backroom vault is back in balance with the authorized till cash amount (see BPPM 30.51).

1.2.d Summary

To summarize, an overage adds money to the backroom till cash vault and a shortage takes money out of the backroom till cash vault.

1.2.e Posting Overages and Shortages

There are times when a department investigates overages and shortages but is unable to find and correct the errors. This leaves the backroom vault out of balance by the amount of the unfound errors. The department must record uncorrectable error amounts in the accounting system using source 490, in accordance with state of Washington guidelines. (SAAM 85.20.10d)

1.2.e.i Posting an Overage

The department must deposit uncorrectable overage money using source-subsource 490-10 when the amount reaches $25.00 and/or at least monthly for amounts less than $25.00. The department processes a receipt in the point-of-sale system using source 490-10 and adds the amount from the backroom till cash vault into the day’s deposit. This brings the backroom vault into balance with the original authorized till cash amount. The department records the transfer of this amount on the vault log sheet, indicating that the vault is back in balance.

1.2.e.ii Posting a Shortage

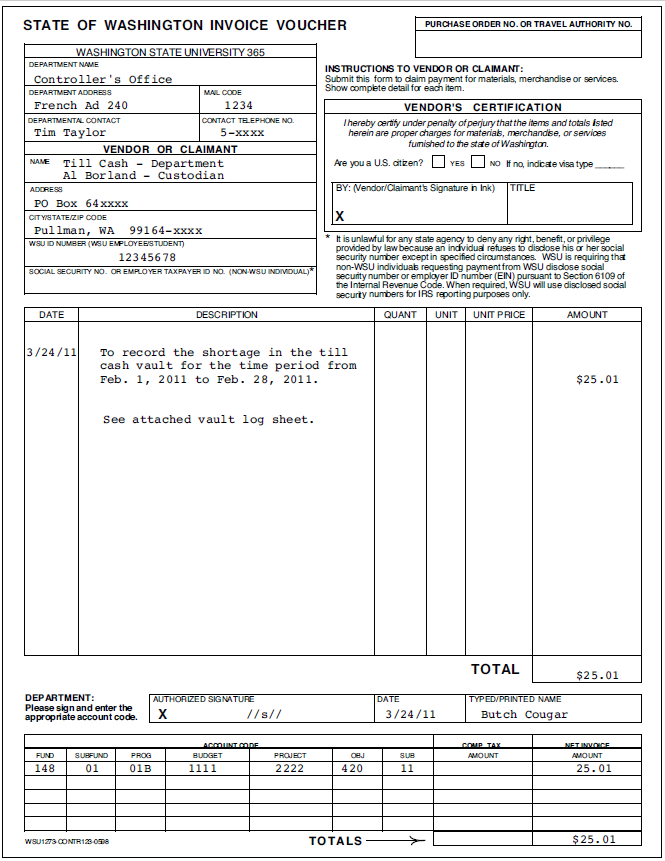

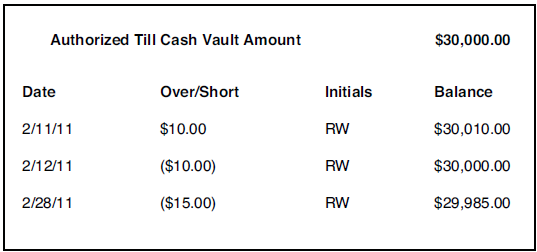

A shortage occurs when the backroom vault contains less money than the authorized till cash amount. The department must post the shortage using source-subsource 490-11 when the amount reaches $25.00 and/or at least monthly for amounts less than $25.00. The department completes a State of Washington Invoice voucher payable to the till cash custodian describing the dates that are covered and using source-subsource 490-11 to account for the shortages (see Figure 3). To obtain a State of Washington Invoice Voucher, see BPPM 30.45. The department must attach a copy of the vault log sheet (see Figure 4) to the invoice voucher. The department sends the completed invoice voucher with attached vault log sheet to the Revenue Section of the Controller’s Office; mail code 1025.

1.2.e.iii WSU Pullman Departments

The Revenue Section of the Controller’s Office generates a check payable to the requesting WSU Pullman department’s till cash custodian and holds it for pickup. The till cash custodian picks up the check at the check distribution desk in General Accounting and may cash the check at the Cashier’s Office. The till cash custodian adds the funds back into the backroom vault to bring it into balance with the authorized till cash amount. The department records the transfer of this amount on the vault log sheet, showing that the vault is back in balance.

1.2.e.iv Non-Pullman Departments

The Revenue Section of the Controller’s Office generates and mails a check payable to the requesting non-Pullman department’s till cash custodian, who cashes the check at a local bank. The till cash custodian adds the funds back into the backroom vault to bring it into balance of the authorized till cash amount. The department records the transfer of this amount on the vault log sheet, showing that the vault is back in balance.

1.2.f Records Retention

The department retains the vault log sheets with the cash register reconciliation records, in accordance with the retention period specified on the All-University Records Retention Schedule (see BPPM 90.01).

_______________________

Revisions: See BPPM 30.53 revision history.