University Policies and Procedures Manual (previously Business Policies and Procedures Manual)

Cash Registers

UPPM 30.59

For more information contact:

Controller’s Office

509-335-2024

Contents

Form: Daily Reconciliation Sheet

1.0 Overview

Departments which use cash registers must maintain complete records of cash register activity. Departments are responsible for closing out each register at the end of the business day and completing a balance reconciliation for each register.

2.0 Cash Register Requirements

In order to maintain complete activity records, cash registers used by University departments must have all of the following:

- One cash drawer per cashier or one cash register per cashier.

- The ability to record the cashier identification name or number for each transaction.

- A cash register tape and a journal tape which record all transactions.

- A key which enables readings or totals of receipts-to-date to be taken during the business day.

- A Grand Total of cumulative sales which cannot be reset to zero or a continuous transaction counter.

- A void transaction key on the register or departmental procedures in place to track voided transaction numbers.

- The ability to show money totals by type, e.g., cash, check, bankcard, CougarCard.

3.0 Balance Cash Register

Follow the procedures below to balance the cash register at the end of each business day.

3.1 Ring Out Register

Total and close out (“ring out”) the cash register.

3.2 Reconciliation Sheet

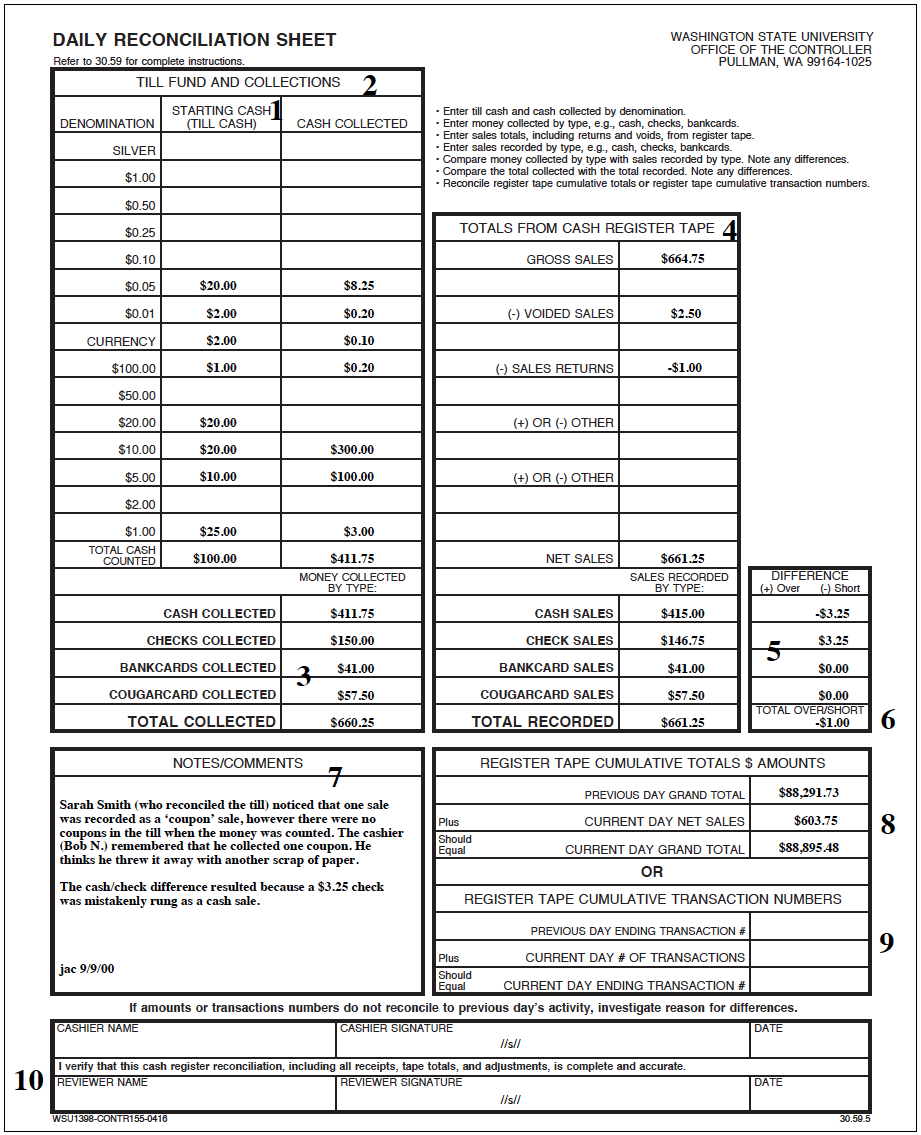

Use a daily reconciliation sheet to compare and balance the register receipts and adjustments against the money (e.g., cash, checks, bankcard receipts) on hand at the end of the day. Departments may create daily reconciliation sheets or use the Daily Reconciliation Sheet as needed. The instructions for completing the Daily Reconciliation Sheet are numerically keyed to numbers on the sample in Fig. 1.

3.2.a Starting Cash (Till Cash)

Remove the till cash before counting the day’s receipts (see UPPM 30.51).

3.2.b Cash Collected

After the till cash is accounted for, list the cash collected, including totals of each denomination.

3.2.c Total Collected by Money Type

List the money collected by type, e.g., cash, checks, bankcard, and CougarCard. Indicate the total collected for the day.

3.2.d Totals from Cash Register Tape

On the other side of the page, list the daily cash register tape totals and any adjustments.

3.2.d.i Net Sales / Gross Sales

Compare the amount of net sales and gross sales (if applicable) showing on the register tape. Note the source of any differences (voided sales, sales returns, and/ or other credits). These adjustments should be accounted for and documentation supporting the adjustments should be retained.

Voided Sales

A supervisor must initial approval for voided sales transactions. The voided sales slip must be attached to the daily reconciliation sheet along with the original sales slip.

3.2.d.ii Sales Recorded by Type

List the sales recorded by type on the register tape, e.g., cash sales, check sales, bankcard sales.

3.2.e Money Collected by Type / Sales Recorded by Type

Compare the amounts of money collected (e.g., cash, checks, bankcards, CougarCards), to the sales listed by money type on the register tape. Investigate and note any differences.

3.2.f Total Recorded / Total Collected

Compare the amount of total sales recorded on the cash register daily tape to the total collected. Investigate and attempt to resolve any differences. If any difference cannot be resolved, write the amount over or short on the reconciliation sheet.

3.2.g Notes/Comments

Describe any differences investigated, attempts to resolve the differences, and any adjustments made to the sales totals and/or totals of money collected.

3.2.h Grand Total

Ensure that the Grand Total from the previous day’s cash register tape plus the current day’s net sales are equal to the Grand Total on the current day’s cash register tape. Note the result of the comparison on the reconciliation sheet. Write the ending Grand Total from the previous day on the current day’s reconciliation sheet.

3.2.i Ending Transaction Number

If cumulative totals are not kept, compare the previous day’s ending transaction number plus the current day’s number of transactions to the current day’s ending transaction number. Write the ending transaction number from the previous day on the current day’s reconciliation sheet.

3.2.j Supporting Documentation

Attach the cash register tape and all supporting documents to the Daily Reconciliation Sheet.

3.2.k Approvals

The cashier and a reviewer sign the reconciliation sheet. The reviewer’s signature indicates that he or she has reviewed the reconciliation sheet and that it is correct.

3.3 Records Retention

The reconciliation sheet and attachments must be retained for six years after the end of the fiscal year. See UPPM 90.01 for records retention requirements.

Note: A department may retain scanned attachment images as the originals, in place of the paper records, if the department is able to ensure that the scanner used produces images that meet state records management requirements. See UPPM 90.21 for further information regarding imaging University records and a link to the state requirements.

3.4 Monitor Sales Adjustments

A supervisor and/or the department manager are to routinely monitor overages, shortages, and other sales adjustments to identify possible problems.

3.5 Refunds

Do not process refunds through the cash register.

3.5.a Cash/Check

Submit a State of Washington Invoice Voucher to the Controller’s Office to refund cash or check purchases (see UPPM 30.45 and 30.55).

3.5.b Credit Card

Note Exception: To make a credit card refund involving a WSU employee, the department must complete an Expense Report business process in Workday. See the Workday Expense Report reference guide for instructions.

4.0 Deposit Money

Someone other than the cashier completes a Record Cash Sale business process in Workday and attaches a copy of the cash register ring-out total tape. See UPPM 30.53 and the Workday Record Cash Sale reference guide for instructions.

_______________________

Revisions: Jan. 2021 (Rev. 560); Apr. 2016 (Rev. 468); Aug. 2001 – new policy (Rev. 191).